1. Introduction to Our guide to Payroll in Malaysia

2. Setting Up a Business

3. Employment Practices

4. Taxation & Social Security

5. Payroll Operations

6. Hiring & Termination

7. Compensation & Benefits

8. Visas & Work Permits

9. Location-Specific Considerations

1. Introduction to Our guide to Payroll in Malaysia

Doing Business in Malaysia

Investing in Malaysia

The Malaysian Investment Development Authority (MIDA) is a subsidiary of the Government. It promotes investments in the manufacturing and services sectors; and advise the Ministry of International Trade and Industry (MITI) on industry matters including the formulation of related policies. MIDA assists companies which intend to invest in the manufacturing and services sectors, as well as facilitates the implementation of their projects. The wide range of services provided by MIDA include providing information on the opportunities for investments, as well as facilitating companies which are looking for joint venture partners.

Basic Facts about Malaysia

| Full Name | Malaysia |

| Population | 35.17 million |

| Capital | Kuala Lumpur |

| Major Language(s) | Malay (official), English, Chinese dialects, Tamil, Telugu, Malayalam |

| GNI Per Capita | USD 11,710 |

| Monetary Unit | 1 ringgit = 100 sen |

| Main Exports | Electronic equipment, mineral fuels, machinery, Optical, technical, and medical apparatus, animal/vegetable fat oil, plastics, aluminum, and iron and steel product. |

| Internet Domain | .my |

| International Dialing Code | +60 |

How to Say

Hello: Halo

Good Morning: Selamat pagi

Good Evening: Selamat petang

Do you speak English?: Anda boleh cakap Bahasa Inggeris?

Goodbye: Selamat tinggal

Thank you: Terima kasih

See You Later: Jumpa lagi

2. Setting Up a Business

Registrations and Establishing a Payroll Entity

Companies are required to register as an employer for tax, Employees Provident Fund (EPF), Social Security Organization (SOCSO), Employment Insurance System (EIS) and Human Resource Development Corporation (HRD Corp) if applicable based numbers of headcount.

Employers must register with the Tax, EPF, SOCSO and EIS when the employee first begins at the company. The principal and immediate employer who employs one or more employees is required to register and contribute monthly to EPF, SOCSO and EIS. Employers must register at the EPF and SOCSO office or through online within 7 days and 30 days respectively from the date the new employee was employed. Whereas employer tax refences (File E Reference No.) can be obtained upon the company being registered under the registrar of company (ROC), where corporate tax and employer tax reference number will be issued by the Inland Revenue Department of Malaysia.

Typical implementation timeline to get a company payroll up and running will be two months including a one-month payroll parallel run. However, implementation duration will vary depending on the complexity of payroll requirements and the headcount to be implemented.

Banking

It is mandatory to make payments from an in-country bank account to employees unless there is a written notice from employee and approval from Government Official Authorities. Generally, banks are open to the public from 09:00AM to 4:30PM, and closed on Saturdays, Sundays and public holidays.

Starting from 2024, the Malaysian government has allowed digital banking as a mode of salary payment. This initiative is part of a broader effort to promote digital financial solutions and enhance financial inclusion across the country.

3. Employment Practices

Working Week

Generally, the working week in Malaysia is Monday to Friday including Half day for Saturday for some employers, however it could vary based on its states. The normal number of hours worked per day in a commercial office is eight hours, Maximum of 45 hours per week.

Employment Law

Annual Leave (Holiday Accrual & Calculation)

Under the Employment Act 1955, minimum annual leave entitlement is based on length of continuous service with the same employer:

Statutory Annual Leave Entitlement:

-

Less than 2 years of service: 8 days of paid annual leave for every 12 months of continuous service

-

2 to less than 5 years of service: 12 days of paid annual leave for every 12 months of continuous service

-

5 years or more of service: 16 days of paid annual leave for every 12 months of continuous service

These are minimum statutory entitlements. Employers may provide more favourable benefits under company policy.

Annual Leave Encashment

Where annual leave encashment is permitted (e.g. upon resignation or termination), calculations are typically based on the ordinary rate of pay.

Encashment Formulae:

Hourly-based calculation

(Basic Salary ÷ (26 days × 8 hours)) × Number of Hours

Daily-based calculation

Basic Salary ÷ 26 days × Number of Days

The Employment Act applies 26 days as the minimum divisor for calculating the ordinary rate of pay for monthly rated employees.

Maternity Leave

Female employees are entitled to 98 consecutive days of maternity leave, regardless of salary level or job category.

Key Provisions:

-

Maternity leave may commence at any time within 30 days before confinement

-

If certified by a registered medical practitioner, maternity leave must commence within 14 days prior to confinement

-

A female employee is not entitled to maternity leave or maternity allowance if, at the time of confinement, she has five (5) or more surviving children

Paternity Leave

Paternity leave is a statutory entitlement under Malaysian employment law. Key Provisions

Duration: 7 consecutive days of paid paternity leave per child

Eligibility conditions:

-

Employee is married to the child’s mother

-

Employee has been employed by the same employer for at least 12 months

-

Employee provides at least 30 days’ notice prior to the expected confinement, or as soon as practicable after the birth

Limit: Applicable for the first 5 births only, regardless of the number of marriages or spouses

This provision supports shared parental responsibility and work life balance for working fathers.

Sick Leave

Employees are entitled to paid sick leave based on length of service with the same employer.

Sick Leave (Without Hospitalisation)

- Less than 2 years: 14 days

- 2 to 5 years: 18 days

- More than 5 years: 22 days

For hospitalisation, employees are entitled to 60 days of sick leave, irrespective of length of service Sick leave eligibility is subject to certification by a registered medical practitioner.

National Service

There are no national service obligations in Malaysia.

Minimum Wage in 2026

As of 2026, Malaysia’s minimum wage remains RM1,700 per month, as set under the Minimum Wages Order 2024 (MWO 2024).

National Public Holidays

| Date | Holiday |

| 1 Jan | New Year’s Day |

| 17 Feb | Chinese New Year (Day 1) |

| 18 Feb | Chinese New Year (Day 2) |

| 21 Mar | Hari Raya Aidilfitri (Day 1) |

| 22 Mar | Hari Raya Aidilfitri (Day 2) |

| 1 May | Labour Day |

| 31 May | Wesak Day |

| 1 Jun | Agong’s Birthday |

| 17 Jun | Awal Muharram |

| 27 May | Hari Raya Haji (tentative) |

| 31 Aug | National Day |

| 25 Aug | Maulidur Rasul |

| 16 Sept | Malaysia Day |

| 14 Nov | Deepavali |

| 25 Dec | Christmas |

4. Taxation & Social Security

Tax, Employee Provident Fund, Social Security & Human Resource Development

Individual Income (Taxes on Employment Income)

Tax Year

The Malaysian tax year runs from 1 January to 31 December, with tax assessed on a calendar-year basis.

Monthly Tax Deduction (MTD / PCB)

Malaysia operates a Monthly Tax Deduction (MTD) system (Potongan Cukai Bulanan – PCB), requiring employers to deduct income tax monthly from employees’ remuneration in accordance with the Income Tax (Deduction from Remuneration) Rules 1994.

MTD Calculation Methods

Employers may compute MTD using IRBM approved methods:

-

Computerised Calculation Method (CCM)

-

IRBM verified payroll software

-

IRBM verified in house or customised payroll systems

The manual PCB table is no longer published, but electronic calculation via IRBM systems remains permissible.

MTD calculations rely on employee submitted personal data. Monthly deductions are computed after considering statutory deductions and declared reliefs, including:

-

Individual relief

-

Spouse relief (if applicable)

-

Child relief

-

EPF contributions

-

Zakat payments (if applicable)

Employer Responsibilities

Employers are required to:

-

Deduct MTD accurately from employee remuneration

-

Submit monthly MTD statements

-

Remit MTD payments to IRBM by the 15th day of the following month

If the 15th falls on a weekend or public holiday, payment must be made on the next working day.

Penalties for Non Compliance

Failure to deduct, submit, or remit MTD may result in:

-

A fine of RM200 to RM20,000

-

Imprisonment of up to six (6) months

-

Or both

as provided under the Income Tax Act 1967.

Income Tax Rates

Resident Individuals

Malaysia applies progressive tax rates, ranging from 0% to 30%, with the maximum marginal rate of 30% applying to chargeable income exceeding RM2 million.

Non Resident Individuals:

-

Taxed at a flat rate of 30%

-

No entitlement to personal reliefs or rebates

-

Applicable to income earned or derived from Malaysia only

An individual is generally regarded as non resident if present in Malaysia for less than 182 days in a calendar year, subject to statutory exceptions.

Individual Tax Filing Obligations

Employer

Borang E is an annual tax return that every employer in Malaysia must submit to LHDN (Inland Revenue Board of Malaysia) by 31st March. It declares:

-

Employer details, and

-

Total employees (including those with no PCB),

-

Confirmation that Form EA has been prepared and issued to employees.

Even if no tax was deducted (PCB = nil), Borang E must still be filed.

Failure to submit Borang E by 31 March may result in:

-

Fine: RM200 – RM20,000

-

Imprisonment: Up to 6 months

-

Or both (under Section 120(1), Income Tax Act 1967)

Each employee/employer is responsible for filing their annual individual income tax return:

| Category | Form | Deadline |

| Employment income only | Form BE | 30 April (manual) / 15 May (e Filing) |

| With business income | Form B | 30 June (manual) / 15 July (e Filing) |

| Non resident individuals | Form M | 30 April |

| Employer declaration to LHDN | Form E | By 31 March |

Tax Reliefs, Deductions & Rebates (Form TP1)

Employees may submit Form TP1 to their employer to declare eligible tax reliefs and rebates for MTD adjustment purposes, resulting in lower monthly deductions.

Key points:

-

TP1 does not need to be submitted to IRBM

-

Employers must process the amounts as declared

-

Employers are not responsible for verifying the accuracy of employee claims

-

Employees must retain supporting documents for up to seven (7) years

Common TP1 claims include:

-

EPF and life insurance

-

Medical and education expenses

-

Lifestyle and childcare reliefs

-

Parental care reliefs

For more information, please refer to the Inland Revenue Board of Malaysia website here.

There are three mandatory statutory contributions:

Employee Provident Fund (EPF)

The Employees Provident Fund (EPF) administers Malaysia’s compulsory retirement savings scheme. It is a statutory body established under the Employees Provident Fund Act 1991 (Act 452) to provide retirement benefits through systematic savings and investment management. Members are entitled to withdraw their accumulated savings upon reaching the age of 55, subject to applicable withdrawal rules.

Coverage and Membership

EPF membership is:

-

Mandatory for Malaysian citizens and permanent residents employed under a contract of service

-

Mandatory for non Malaysian employees with valid work passes, effective October 2025 wages, at a prescribed lower contribution rate

-

Voluntary for self employed individuals and certain categories of workers

The following groups are generally excluded from mandatory EPF contributions:

-

Domestic servants employed in private households

-

Self employed persons (unless they opt in)

-

Employees below the minimum contribution age

-

Certain expatriates or foreign workers prior to October 2025 policy changes

Civil servants are covered separately under the pension scheme, while voluntary private retirement schemes remain available for eligible individuals.

EPF Contributions

An EPF contribution consists of employer and employee portions credited monthly into the member’s EPF accounts. Contributions are calculated based on monthly wages as defined under the EPF Act and must be remitted by the 15th day of the following month.

Contribution Rates (Employees below 60 years old)

Malaysian Citizens & Permanent Residents

-

Monthly wages of RM5,000 and below

-

Employee: 11%

-

Employer: 13%

-

-

Monthly wages exceeding RM5,000

-

Employee: 11%

-

Employer: 12%

-

Non Malaysian Employees (members registered on or after 1 August 1998)

-

Employee: 2%

-

Employer: 2%

This applies to foreign employees with valid work permits or passes, excluding foreign domestic helpers, and is mandatory for wages from October 2025 onwards.

Employer Obligations

Employers are required to:

-

Register as an EPF employer and register eligible employees

-

Deduct the employee’s EPF contribution from wages

-

Pay both employer and employee contributions monthly

-

Keep accurate payroll and contribution records as required under law

Failure to comply may result in penalties under the EPF Act 1991.

Adjustments to Contribution Rates

The employee’s statutory contribution rate is currently fixed at 11%. However:

-

The Government may temporarily reduce the employee contribution rate through gazette notification during periods of economic hardship

-

Any such changes would apply prospectively and be announced officially

Voluntary and Additional Contributions

Employees are allowed to:

-

Increase their EPF contribution above 11%, subject to EPF rules and payroll implementation requirements

-

Make voluntary self contributions under i Simpan

-

Make additional contributions through i Topup, including top ups by employers or individuals

Terms, caps, and eligibility conditions apply, and participation is subject to EPF approval and operational guidelines

For more information, please refer EPF website at https://www.kwsp.gov.my

SOCSO (Social Security Organisation)

The Social Security Organisation (SOCSO), also known as PERKESO, is a statutory body established to administer, enforce, and implement the Employees’ Social Security Act 1969 (Act 4) and the Employees’ Social Security (General) Regulations 1971. SOCSO provides social security protection to employees through a social insurance system encompassing medical care, cash benefits, rehabilitation, provision of artificial aids, and financial protection for insured persons and their dependants.

SOCSO Protection Schemes

SOCSO administers two main social protection schemes under Act 4:

1. Employment Injury Scheme

This scheme provides protection for employees in respect of:

-

Industrial accidents occurring in the course of employment

-

Commuting accidents (travelling to and from work)

-

Emergency and work related accidents

-

Occupational diseases

Benefits include medical treatment, temporary and permanent disablement benefits, dependants’ benefits, and rehabilitation services.

2. Invalidity Scheme

This scheme provides long term financial assistance to employees who suffer invalidity or death from causes not related to employment. Benefits include:

-

Invalidity pension

-

Survivors’ pension

-

Funeral benefit

Coverage and Mandatory Contributions

Any employer employing one or more employees is required to register with SOCSO and make monthly contributions for all eligible employees under Act 4. Coverage generally includes:

-

Permanent, temporary, and contract employees

-

Part time employees

-

Local and foreign employees employed under a contract of service

Certain public sector employees on contract or temporary appointments are now covered under Act 4, although employees under the public pension scheme remain excluded, and such employees are not covered under the Employment Insurance System (EIS).

SOCSO Contribution Rates (2026)

SOCSO contributions are table based, subject to a salary ceiling of RM6,000 per month, which has applied since 1 October 2024 and remains in force for 2026.

For employees below 60 years of age (Category 1 – Employment Injury + Invalidity Schemes):

-

Employee contribution: approximately 0.5% of monthly wages

-

Employer contribution: approximately 1.75% of monthly wages

The exact contribution amounts are determined using SOCSO’s prescribed contribution tables rather than a flat percentage.

For employees aged 60 and above or in specific circumstances (Category 2 – Employment Injury Scheme only):

-

Employer contribution only applies, based on SOCSO’s tables

-

No employee contribution is required

Payment Deadline and Penalties

Employers are required to remit SOCSO contributions by the 15th day of the month following the wage month. For example, January contributions must be paid no later than 15 February.

Late Payment Charges

- Interest on late payments is charged at 6% per annum, calculated daily

- A minimum charge of RM5 per month applies if the calculated amount is less

Non compliance may also expose employers to compounding, prosecution, fines, or imprisonment under the Employees’ Social Security Act 1969.

Salary Ceiling Increase (Still Applicable in 2026)

Effective 1 October 2024, the insured salary ceiling for SOCSO was increased from RM5,000 to RM6,000 per month. As a result:

-

Contributions for salaries above RM6,000 are capped at RM6,000

-

Employees earning between RM5,000 and RM6,000 receive enhanced benefit protection

-

SOCSO cash benefit rates have increased by up to 20.2%

This change applies to both Malaysian and foreign employees and remains applicable throughout 2026.

Income Tax Relief

Employees are eligible to claim personal income tax relief of up to RM350 per annum for their combined SOCSO and EIS contributions, subject to Inland Revenue Board guidelines and annual tax filing requirements. For more information, please click here.

Employment Insurance System (EIS)

The Employment Insurance System (EIS) is established under the Employment Insurance System Act 2017 (Act 800) and is administered by the Social Security Organisation (SOCSO / PERKESO).

EIS provides temporary financial assistance, re employment support, and labour market interventions to insured persons who have lost their employment, with the objective of promoting active labour market policies and faster re integration into the workforce.

EIS is not limited to cash benefits upon retrenchment. It also provides comprehensive employment related support services, including:

-

Job seeking and job matching assistance via MYFutureJobs

-

Re employment allowance

-

Reduced income allowance (for those working reduced hours or wages)

-

Training allowance and reskilling programmes

- Career counselling and employability services

Coverage and Eligibility

An employer who employs one or more employees is required to:

-

Register under the Employment Insurance System, and

-

Make monthly EIS contributions for all eligible employees.

EIS coverage applies to:

-

Employees aged 18 to 60 years

-

Malaysian and eligible foreign employees employed under a contract of service

-

Permanent, contract, and temporary employees

Employees aged 60 and above, public sector employees under pensionable service, and certain prescribed categories are excluded from EIS coverage under Act 800.

Contribution Rates (2026)

Contributions to EIS are calculated as a percentage of the employee’s monthly wages, subject to the statutory wage ceiling.

-

Total contribution rate: 0.4% of monthly wages

-

Employer contribution: 0.2%

-

Employee contribution: 0.2%

-

Contributions are:

-

Shared equally between employer and employee

-

Capped at a monthly salary of RM6,000, effective 1 October 2024 and continuing to apply in 2026

For employees earning more than RM6,000, both employer and employee contributions are calculated based on the maximum insurable wage of RM6,000 only.

Employer Obligations and Payment Deadline

Employers are responsible for:

-

Registering employees under EIS

-

Deducting the employee’s share of EIS contribution from wages

-

Remitting both employer and employee contributions to SOCSO

EIS contributions must be paid by the 15th day of the month following the wage month.

Late payments are subject to:

-

Interest at 6% per annum, calculated daily

-

A minimum late payment charge of RM5 per month if the calculated amount is lower

Failure to comply may result in enforcement action under the Employment Insurance System Act 2017.

Human Resource Development Fund

The Human Resource Development Corporation (HRD Corp) is a statutory agency under the Ministry of Human Resources Malaysia, established pursuant to the Pembangunan Sumber Manusia Berhad Act 2001 (PSMB Act 2001). HRD Corp is responsible for driving workforce upskilling and talent development through the collection of a statutory levy from employers and the redistribution of these funds as financial assistance for employee training and development programmes.

Employers who contribute to the HRD levy are eligible to claim training costs, subject to HRD Corp’s guidelines and available levy balances.

Employer Registration and Levy Requirement

Under the PSMB Act 2001, employers are categorised based on the size of their Malaysian workforce:

Mandatory Registration

-

Employers with 10 or more Malaysian employees

-

Required to register with HRD Corp

-

Required to contribute 1.0% of monthly wages plus fixed allowances for each eligible employee

Voluntary Registration

-

Employers with 5 to 9 Malaysian employees

-

Registration is optional

-

If registered, contributions are required at 0.5% of monthly wages plus fixed allowances for each eligible employee

Employers with fewer than 5 Malaysian employees are not required to register or contribute.

Levy Calculation

The HRD levy is calculated based on:

-

Basic salary, and

-

Fixed allowances, such as housing or cost of living allowances

Variable or non fixed payments (e.g. bonuses, commissions, overtime, travel allowances) are excluded from the levy calculation.

Levy Formula: (Basic Salary – Unpaid Leave) + Fixed Allowances × Applicable Levy Rate

Levy Payment and Compliance

-

Levy payments must be made monthly, no later than the 15th day of the following month

-

Payments are made via HRD Corp’s e TRiS system

Late Payment Consequences

Failure to pay the levy within the stipulated timeframe may result in:

-

Late payment interest at 10% per annum

-

A minimum interest charge of RM5

-

Possible enforcement action under the PSMB Act 2001, including:

-

Fines up to RM20,000

-

Imprisonment of up to two (2) years

-

Or both

-

Use of HRD Levy

Employers may utilise their HRD levy to claim reimbursement for:

-

Course and trainer fees

-

Training materials

-

Certification costs

-

Selected accommodation and transportation expenses (subject to HRD Corp approval and scheme rules)

Unutilised levy balances are subject to forfeiture after the prescribed retention period in accordance with HRD Corp circulars.

Special Update for 2026 – Education Sector Levy Exemption

Registered employers classified under the Education Industries (including private schools, training centres and private higher learning institutions) are granted a one year exemption from HRD levy payments from January 2026 to December 2026.

Key points:

-

No levy payment is required during the exemption period

-

Employers may continue to apply for training grants and utilise existing levy balances

-

Levy contributions will resume from January 2027

For more information, please click here.

PTPTN (National Higher Education Fund Corporation)

The National Higher Education Fund Corporation (PTPTN) was established in 1997. The PTPTN Education Financing Scheme was established to provide finance to students that are perusing studies in local institutions of higher education. The funding provided will enable students to pay for all or some of their course fees and their cost of living throughout their studies.

The main functions of PTPTN are;

-

To manage funds for higher education purposes and collecting repayments of financing

-

To provide and manage education savings schemes

-

To perform any other duties as per written law

The recipient of the finance is responsible for repaying the total amount disbursed by PTPTN, including other costs such as fees, insurance coverage, stamp duty and miscellaneous payments as stated in the Letter of Offer. Repayment of the loan will begin twelve months after the completion of the student’s studies.

An employer is only affected when:

-

An employee submits a PTPTN salary deduction instruction, or

-

The employer receives an official PTPTN deduction notice / consent form

Without this, PTPTN is not a mandatory deduction like EPF, SOCSO, EIS, or PCB.

Process:

-

Employee registers for salary deduction (Potongan Gaji) with PTPTN

-

PTPTN issues a deduction instruction (amount & reference)

-

Employer deducts the stated amount monthly. Deduction amount must match PTPTN instruction and it will be reflected as PTPTN Deduction in payslip.

- Employer remits payment to PTPTN

Zakat

Zakat is a charitable donation to assist the less fortunate; all of the collected payments will be distributed to different channels and handed to those that need it most. Zakat is only applicable to Muslim employees and it is not compulsory via payroll deduction. It is also eligible for monthly tax (MTD) net off.

ASB

Amanah Saham Bumiputera (ASB) is a unit trust fund managed by Amanah Saham Nasional Berhad (ASNB), a subsidiary of Permodalan Nasional Berhad (PNB). ASB provides a stable and reliable investment option, especially for Bumiputera investors looking for long-term financial growth.

From an employer’s payroll and compliance standpoint:

-

ASB deduction is considered a voluntary investment arrangement

-

It is treated as a third‑party payment

-

There is no statutory obligation under Malaysian labour or tax law for employers to facilitate ASB deductions

The employer has the right to approve or reject ASB salary deduction requests.

It is reasonable and acceptable for an employer to:

-

Decline ASB deduction requests where only a minority of employees (e.g. 1–2 persons) opt in

-

Consider administrative cost, payroll system limitations, and operational burden

- Standardise payroll deductions to statutory items only

Reporting: Monthly Reporting

Income Tax (MTD / PCB)

Payment Deadline: 15th day of the following month. Employers are required to deduct and remit Monthly Tax Deduction (MTD / PCB) to the Inland Revenue Board of Malaysia (IRBM). Key forms and reporting:

-

CP39 – Statement of Monthly Tax Deduction (MTD)

-

CP22 – Notification of New Employee (mandatory online submission for new joiners)

Retrenchment / Retirement / Leaving Malaysia

The following notifications must be submitted to IRBM in cessation related cases:

-

CP21 – Notification of Employee Leaving Malaysia (tax clearance required)

-

CP22A – Notification of cessation of employment due to resignation, retrenchment, retirement, or termination with substantial termination payments

Employee Provident Fund (EPF / KWSP)

Payment Deadline: 15th day of the following month. Employers must:

-

Register for i Akaun (Employer) – mandatory for all employers

-

Submit monthly EPF contributions online

Employer registration:

-

New employers: Form KWSP 1 and KWSP 1(i)

-

Existing employers: Form KWSP 1(i) only

SOCSO (PERKESO)

Payment Deadline: 15th day of the following month. SOCSO contributions are submitted through the PERKESO Assist Portal. New employee registration:

-

Form 2 (SOCSO) – New employee registration (A copy of the employee’s Identity Card is required)

Employment Insurance System (EIS / SIP)

Payment Deadline: 15th day of the following month. EIS contributions are submitted through the PERKESO Assist Portal. Employee registration:

-

SIP Form 2 – New SIP member

-

SIP Form 2A – Existing SIP member

HRD Levy (HRD Corp)

Payment Deadline: 15th day of the following month. Levy contribution requirements:

-

10 or more Malaysian employees: 1.0% of monthly wages plus fixed allowances

-

5 to 9 Malaysian employees: Optional registration at 0.5% of monthly wages plus fixed allowances

Registered employers must remit levy payments monthly via the e TRiS system.

Annual / Year End Reporting

Employer Reporting

Form E – Employer Annual Return

-

Deadline: 31 March of the following year

-

Purpose: Annual declaration of employee remuneration details

-

Submission: Mandatory electronic filing via MYTax / e E (https://ez.hasil.gov.my)

Form EA (formerly CP8A) – Employee Remuneration Statement

-

Deadline: 28 February of the following year

-

Purpose: To support employees’ individual tax filing

-

Distribution: Provided to each employee by 28 February (Electronic copies are acceptable; signatures are not required)

New Employee Onboarding – Mandatory Notifications

Employers must submit the following upon hiring a new employee in Malaysia:

-

SOCSO Form 2 – SOCSO registration

-

SIP Form 2 – EIS registration

-

CP22 – Notification of new employee to IRBM (mandatory online)

Required employee documents:

-

Completed personal details form

-

Copy of Identity Card

- Form TP3 – Prior employment income details (if employed in Malaysia earlier in the same assessment year)

Effective 1 September 2024, Form CP22 must be submitted online via e CP22 on the MYTax portal.

Employee Leavers & Tax Clearance

Employers must withhold final salary and payments (including bonus, gratuity, or other termination benefits) pending tax clearance for the following cases:

-

Resignation

-

Retirement

-

Retrenchment

-

Employee leaving Malaysia

Leaving Malaysia

-

Employee must submit Form CP21

-

Employer releases final payment only upon receipt of tax clearance letter from IRBM

- Any tax shortfall will be deducted prior to payment release

Summary Timeline (Quick Reference)

| Item | Reporting Cycle | Deadline |

| PCB/CP39 | Monthly | 15th |

| EPF | Monthly | 15th |

| SOCSO | Monthly | 15th |

| EIS | Monthly | 15th |

| HRD LEVY | Monthly | 15th |

| FORM EA | Annual | 28 Feb |

| FORM E | Annual | 31 Mar |

| Employee Tax Filling | Annual | 30 Apr/30 Jun |

5. Payroll Operations

Payroll

It is legally acceptable to provide employees with payslips in either hard copy or online.

Reports

Employer must keep and retain payroll records for seven (7) years and make it readily accessible to the Inland Revenue Board of Malaysia and other statutory bodies when needed commonly for audit purpose.

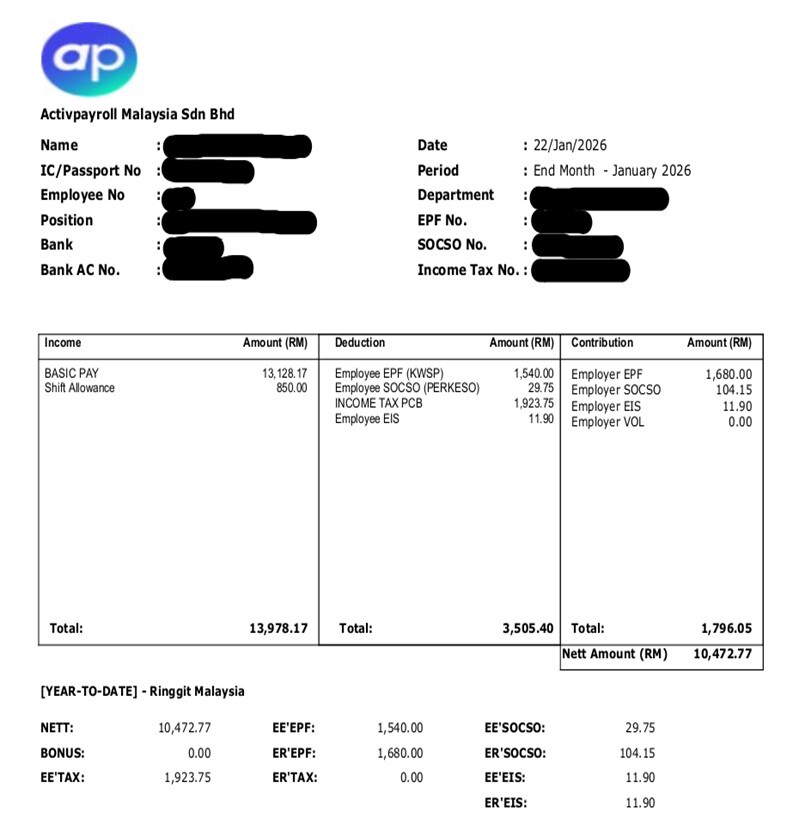

Payslip Example

The issuance of payslip is mandatory as per the Malaysia Employment Act 1955. All employers shall furnish every employee employed by him in a statement relating to the details of earnings and deductions during the wage period.

6. Hiring & Termination

New Employees

Employers must register new employees with EPF, SOCSO, and EIS on or before their first day of work. Required documentation includes:

- Completed registration forms (e.g., KWSP 3, PERKESO 2, EIS 1)

- Photocopy of IC (identity card) or passport

Leavers

Upon termination, employers must notify the tax authorities via:

- Form CP22A for resignation or termination

- Form CP21 for expatriate departure

Termination Notice

Statutory notice periods are:

- Less than 2 years: 4 weeks

- 2 to 5 years: 6 weeks

- More than 5 years: 8 weeks

Termination can occur via resignation, dismissal, or mutual agreement. Final salary payments should account for unused leave and prorated salary.

7. Compensation & Benefits

Employee Benefits

Employee who has Benefits-in-Kind (BIK), Value of Living Accommodation (VOLA) and allowable tax deductions and rebates through submission of Form TP1 to the employer, can be subject to monthly tax deduction (MTD) calculation, instead of year end declaration of the employees’ earnings [via Form BE (without business income) or Form B (with business income)].

Expenses

Employee expenses can be integrated into payroll in a form of allowances. It is at the discretion of the employer to identify what kind of allowance will apply.

8. Visas & Work Permits

Foreign nationals working in Malaysia must hold a valid immigration status and work authorisation issued by the Malaysian authorities. Depending on the nature and duration of the assignment, foreign employees may be issued with permanent residence, employment passes, or temporary work permits.

While foreign nationals may apply for Permanent Residence (PR) subject to eligibility criteria, the Employment Pass remains the most common category used for corporate hires and intra company transfers.

Common Work Authorisation Categories

1. Employment Pass (EP)- Issued to foreign nationals employed by a locally registered sponsoring entity

- Salary must be paid in Malaysia

- Applicable for professional, managerial, executive, and technical roles

- Validity is granted based on Employment Pass category and may be issued for up to several years, subject to renewal and prevailing immigration policy

- Applications and renewals are processed through the Expatriate Services Division (ESD)

- For short term assignments, generally less than 12 months

- Employee remains on home country payroll

- No local employment is created in Malaysia

- Commonly used for:

- Technical assistance

- Knowledge transfer

- Training or consultancy assignments

- Applicable for temporary assignments, typically ranging from 6 months up to a maximum of 12 months

- Salary must be paid by the Malaysian sponsoring entity

- Commonly used for:

- Project based roles

- Semi skilled or technical assignments of limited duration

Permanent Residence (PR)

Foreign nationals may apply for Permanent Residence under specific schemes administered by the Malaysian authorities.

PR holders are not required to hold a work permit, but remain subject to Malaysian employment, tax, and statutory contribution laws.

Employer Registration & Statutory Notifications (Where applicable)

Upon commencement of employment, employers are responsible for submitting the following registrations and notifications:

-

Form CP22 – Notification of New Employee (Income Tax registration with IRB; mandatory online submission)

-

EPF (KWSP) Form 3 – Application for member registration and amendment of member particulars

Expatriate New Employee – Payroll & HR Documentation

To establish payroll records and ensure compliance, employers must retain the following documents for expatriate employees:

-

Completed personal details form

-

Passport copy (bio data and photograph page)

-

Copy of valid work authorisation (Employment Pass / Professional Visit Pass / Permanent Residence)

-

Form TP3, if the employee was previously employed in Malaysia within the same tax assessment year

-

Signed employment contract

These records must be retained in accordance with Malaysian employment, tax, and audit requirements.

9. Location-Specific Considerations

Payroll Services in Malaysia

Looking for payroll support in Malaysia? Our global payroll specialists help businesses manage payroll processing, compliance requirements and employee payments across Malaysia and throughout the Asia-Pacific region.

Learn more about how we support organisations operating in Malaysia and across APAC.

Discover how global EOR services enable businesses to hire, onboard and manage employees compliantly across multiple countries.