1. Introduction to Our guide to Payroll in Greece

2. Setting Up a Business

3. Employment Practices

4. Taxation & Social Security

5. Payroll Operations

6. Hiring & Termination

7. Compensation & Benefits

8. Visas & Work Permits

9. Location-Specific Considerations

1. Introduction to Our guide to Payroll in Greece

Doing Business in Greece

Investing in Greece

Greece is an appealing investment location because it offers businesses a wide variety of investment opportunities. Greece is a natural gateway to more than 140 million consumers in South East Europe and the Eastern Mediterranean. It is a hub of diverse emerging markets, with strong demands in consumer goods, infrastructure and modernization, technology and innovation networks, energy and tourism development.

Basic Facts about Greece

General Information

Full Name:

The Hellenic Republic

Population: 10.72 million (World Bank, 2020)

Capital: Athens

Major Language(s): Greek

Major Religion(s): Christianity

Monetary Unit: Euro

Main Exports: Textiles and clothing, food, oil products

Internet Domain: .gr

International Dialing Code: +30

How To Say

Hello: Geia sas

Good Morning: Kalimera

Good Evening: Kalispera

Do you speak English? Milate Agglika?

Goodbye: Antio

Thank you: Efharisto

See You Later: Tha ta poume meta!

2. Setting Up a Business

Registrations and Establishing an Entity

In order to process payroll in Greece, a company must have a legal entity set up. The estimated completion of this process will depend on the type of company (e.g. IKE, Ltd, A.E.) and it will take approximately two months to complete.

In order for a company to start processing payroll in Greece, a company will need a tax number (obtained from the tax authorities) and an AME number (obtained from the social contributions authorities). It is estimated that registering with the tax and social contributions authorities will take five working days.

No license is necessary before making any tax/social security fillings on behalf of a client. A proxy will be required; however, the client can provide the authorization for this.

Banking

Usually, banks are open Monday to Thursday 08:00 to 15:00 and 08:00 to 14:30 on Fridays.

It is not mandatory for employees to be paid via Greek bank account, it is however mandatory for the authorities (income tax and social contributions) to be paid via a Greek bank account.

3. Employment Practices

Working Week

The working week in Greece is Monday to Friday, with the weekend being Saturday and Sunday.

Employment Law

Holiday Accrual / Calculations

Employees working a five‑day week are entitled to a minimum of 20 working days of paid annual leave in their first year of employment, 21 working days in the second year, and 22 working days from the third year onward. Employees are entitled to 25 working days of paid leave after completing either 10 continuous years with the same employer or a total of 12 years of employment history. After 25 years of employment, leave entitlement increases to 26 working days.

Maternity Leave

Female employees are entitled to 56 days of maternity leave before the expected date of childbirth and 63 days after childbirth. The employer is required to pay salary and social security contributions for the first 30 days of maternity leave if the employee has completed at least one year of service, or for 15 days if the employee has less than one year of service. The remaining maternity allowance is paid by the social security authority (e‑EFKA).

Following the statutory maternity leave, mothers are entitled to a special nine‑month maternity protection leave, paid by the state. Dismissal is prohibited for at least 18 months after childbirth. Upon returning to work, mothers are entitled to reduced working hours, either by one hour per day for two and a half years, or by an alternative reduced schedule if agreed with the employer.

Paternity Leave

Fathers are entitled to 14 working days of paid paternity leave following the birth of their child.

Sickness

In the event of illness, the employee must submit a medical certificate issued by a licensed physician. Sick leave is generally unpaid for the first three days unless otherwise agreed. From the fourth day onward, sickness benefits are paid by e‑EFKA, with possible employer supplementation depending on applicable collective agreements.

National Service

Greek males between the ages of 19 and 45 are required by law to complete compulsory military service of at least nine months. This obligation applies regardless of residence or citizenship status. Employers are not required to pay salary during military service.

4. Taxation & Social Security

Tax & Social Security

The tax year in Greece runs from 1 January to 31 December each year.

Income Tax

Employers in Greece are responsible for withholding personal income tax and employee social security contributions, and for paying employer social security contributions to the unified social security fund (e‑EFKA).

Individuals who are tax residents of Greece are taxed on their worldwide income, while non‑residents are taxed only on income sourced in Greece. Income is classified into categories, and total taxable income is calculated as the aggregate of each category.

Employment and Pension Income:

|

Income Bracket (Euro) |

Tax Rate (%) |

|

0 - 10,000 |

9 |

|

10,0001 - 20,000 |

22 |

|

20,0001 - 30,000 |

28 |

|

30,0001 - 40,000 |

36 |

|

Over 40,000 |

44 |

Income tax withholding on salaries is declared and paid on a bimonthly basis, no later than the end of the second month following the month of payment, through the AΑΔΕ electronic system.

Employers must also submit an annual statement summarizing total employment income and taxes withheld for the year.

Late filing or payment is subject to administrative penalties and statutory interest, in accordance with Greek tax procedure law.

Social Security

All salaries in Greece are subject to mandatory social security contributions. Greece operates a unified social insurance system administered by e‑EFKA (Electronic National Social Security Fund), which replaced former funds such as IKA, OAEE and ETAA.

Employees in dependent employment, including full‑time and part‑time workers, are insured with e‑EFKA. Coverage applies regardless of the number of employers, contractual form, or sector, subject to specific statutory exceptions.

The social insurance contributions are as follows:

h2|

IKA |

Tax Rate |

|

Employee |

13.37% |

|

Employer |

21.79% |

Contributions are calculated on the gross salary, up to a statutory maximum insurable earnings ceiling.

Reporting and Payment

- Employers must submit a monthly Analytical Periodic Declaration (APD) detailing employee earnings and contributions.

- Social security contributions must be paid by the end of the month following the month of employment.

Late Payment Consequences

Late payment of contributions results in:

- Statutory default interest, calculated monthly

- Administrative penalties, depending on the nature and duration of the breach

- Increased sanctions for repeated or deliberate non-compliance

Reporting

Monthly

At the end of each month, there are a number of documents that must be submitted to the authorities. These include; APD file (IKA file) (Social contributions), income tax declaration and any extra contribution file. Submissions can be made online, or if they are last minute, they must be done in person.

Yearly

The annual Company Income Tax Statement must be submitted via the relevant internet service each year. The deadline varies each year. Employee’s annual statements will include the annual gross and net income of the employees and any withheld tax and social security amounts. The annual statements are generated and provided by 31 March of the following financial year.

5. Payroll Operations

Payroll

Reports

It is legally acceptable to provide employees with online payslips in Greece.

Payroll reports must be kept for at least 10 years.

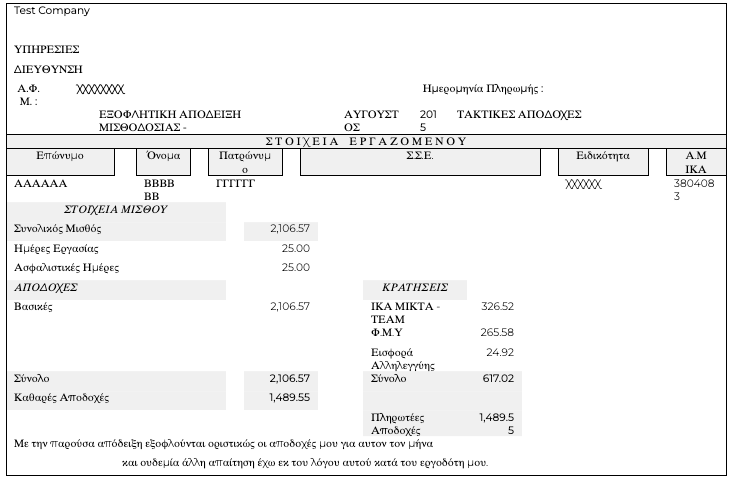

Payslip Example

6. Hiring & Termination

New Employees

All new employees must be registered with the Tax Office and IKA. They must obtain an AMKA (Social Security Number) in person. New starts must be registered before the date of recruitment otherwise, there will be fines.

For any expat new starts, the following documentation is required:

- ID card/passport

- Completion of form M1 and M7

- Utility bill

- Employer confirmation for his/her recruitment

- AMKA confirmation

- A copy of the employee’s Greek bank account details

- Again, the information regarding expat employees must be submitted before their recruitment date otherwise fines will be applicable.

- In order to work in Greece, each employee must have a VAT number. If employees do not have one, they must obtain one from the Greek authorities.

Leavers

When there is a leaver, a termination form must be submitted to the local authorities no later than eighty-four days after the employee’s termination.

If the leaver has been terminated, then payment should be on their last day. If the leaver has resigned, payment will depend on the deadline for each allowance.

7. Compensation & Benefits

Employee Benefits

Expenses

The taxable income in Greece will be established by deducting the following expenses; Social Security Contributions, interest paid for buying a house for the first time and medical care expenses where applicable.

8. Visas & Work Permits

Visas & Work Permits

EU National

All EU nationals must apply for a “Registration Certificate” once they have spent three months in Greece. The Registration Certificate replaces the “Residence Permit” and is obligatory. The new certificate is open dated and will not need to be renewed.

In the case of a working person, the following documents are required when applying for a registration certificate:

- The passport used when the applicant entered Greece

- A statement by the applicant’s duly certified by the local Labour Inspectorate, or a statutory declaration (Ypefthini Dilosi) in Greek specifying the nature and duration of the work to be done by the applicant and confirming local health cover

In the case of the workers family, the following documents are required:

- The passport used when the applicants entered Greece.

- A document issued by the appropriate authority of the country of origin showing their relationship, for example marriage/birth certificates, which will need to be translated into Greek or, alternatively, applicants may sign a statutory declaration (Ypefthini Dilosi) in Greek to confirm the relationship

The “Permanent Residence Certificate” is an optional certificate available to EU nationals. This certificate may be suitable for EU nationals who are married to a Greek citizen or to EU nationals who have made Greece their permanent home. If anyone wants to obtain this certificate, they must prove that they have been a permanent resident of Greece for over five years.

Applications for any of the above certificates should be made to the local Aliens Police or to the local police station closest to the employee’s residence.

Non-EU Citizens

Any non-EU citizen that plans to stay in Greece for more than three months and work must obtain an entry visa. This visa must be obtained before arriving in Greece, usually from the Greek Embassy or Consular in the applicant’s country of residence.

The documents required for applying include;

- A valid passport

- Employment contract

- Proof of adequate medical insurance coverage whilst in Greece

- Criminal background check from the police station nearest the applicant’s residence

Within 30 days of arrival in Greece, the visa holder must apply in person for a residence/work permit at the local municipal office or police station. The type of permit needed will depend on the applicant’s circumstances. It can be valid from one year up to five years.

Before applying for a residence permit, applicants must obtain a tax number and a social security (AMKA).

Application forms for residence permits can be obtained at and submitted to the local municipal office. Applications must be submitted in Greek either in person or by a certified lawyer that has been granted power of attorney.

The documents required to obtain a residence permit include:

- Visa

- Passport (plus photocopies)

- At least two passport photographs

- Certificate of Medical Insurance

- Health Certificate from a state hospital (declaration that the applicant does not have any serious communicable diseases)

- Proof of local address (title deed or rental contract)

- Proof of ability to support oneself - job or resources

- Proof of payment of the required fee to the national tax office (Eforia)

Once the application has been submitted, the applicant will receive a blue form (bebaiosi) as receipt that the application is being processed. The applicant may begin working at this time.

9. Location-Specific Considerations

Further Information

For more information, or assistance with Greece tax enquiries please contact: gi@activpayroll.com

About This Payroll and Tax Overview

Please note that this document gives general guidance only and should not be regarded as an authoritative or complete statement of the law, regulations or tax position in any country. You should always seek specific advice for each specific situation. This document should not be relied upon as professional advice and activpayroll accepts no liability for reliance on its contents.