1. Introduction to Our guide to Payroll in the UK

2. Setting Up a Business

3. Employment Practices

4. Taxation & Social Security

5. Payroll Operations

6. Hiring & Termination

7. Compensation & Benefits

8. Visas & Work Permits

9. Location-Specific Considerations

1. Introduction to Our guide to Payroll in the UK

Doing Business in the UK

Investment in the UK

The UK government provides incentives for foreign investment in key industries to attract foreign companies to invest in the UK. The UK offers investors access to a wealthy and stable economy, supported by a highly educated workforce.

Basic Facts about the UK

Full Name: United Kingdom of Great Britain and Northern Ireland

Population: 67.03 million (Office for National Statistics, 2021)

Capital: London

Major Language(s): English

Major Religion(s): Christianity

Monetary Unit: Great British Pound

Main Exports: Manufactured goods, chemicals, foodstuffs

GNI Per Capita: US $49,470 (World Bank, 2024)

Internet Domain: .uk

International Dialing Code: +44

2. Setting Up a Business

Registrations and Establishing an Entity

Every time a new company starts trading in the UK, this company must be registered as an employer with HM Revenue and Customs (HMRC). This process involves providing HMRC with all the relevant company details, including the trading name of the company, the registered address details etc. for them to recognize you as a trading company. More importantly, this process also gives you the reference numbers to allow you to liaise with HMRC in future, and to ensure that you are given full credit for any payments of Income Tax and National Insurance that you make in the future.

Banking

It is mandatory to make payments to both employees and the authorities from an in-country bank account. Generally, banks are open to the public from 0900 to 1700 Mon-Fri, 0900 to 1500 Saturdays, and closed on Sundays.

3. Employment Practices

Working Week

The working week in the UK is Monday to Friday. The working day for commercial offices is usually eight hours, typically from 0800 or 0900 to 1600 or 1700. Lunch breaks are usually one hour.

Employment Law

Holiday Accrual

Most employees are legally entitled to paid holidays/annual leave. A worker's statutory paid holiday entitlement is 5.6 weeks (28 days for a worker working a five-day week). This can include public and bank holidays. The entitlement for part-time workers is calculated on a pro-rata basis.

Maternity Leave

If an employee is expecting a baby, she may be entitled to Statutory Maternity Pay (SMP). This replaces her normal earnings to help her take time off around the time of the birth.

Whether the employer will have to pay SMP to an expectant employee depends on how long they've worked for that employer and how much they earn.

Payments of SMP count as earnings therefore the employer must deduct tax and National Insurance contributions (NICs) from them in the usual way.

For the first six weeks, the employer must pay the employee SMP at the rate of 90 per cent of their average weekly earnings.

For the next 33 weeks you must pay them the lower of the following:

- £187.18 or 90% of their average weekly earnings, whichever is lower for 2025/2026 and £194.32 or 90% of their average weekly earnings, whichever is lower for 2026/2027

- If the employer’s total National Insurance payments were £45,000 a year or less for the previous tax year, they'll be able to recover 108.5 per cent of the SMP. This is to compensate the employer for the NICs they would have had to pay on the SMP.

- If the employer’s National Insurance payments were more than £45,000 for the previous tax year they will be able to recover 92 per cent of the SMP that they have paid.

- The employer can recover SMP by deducting it from your monthly PAYE (Pay as You Earn) payments. Or you can ask HM Revenue & Customs (HMRC) for funding in advance.

Paternity Leave

You can take either 1 or 2 weeks’ leave. If you choose to take 2 weeks, you can take them together or separately. You get the same amount of leave even if you have more than one child (for example, twins).

A week of leave is the same amount of days that you normally work in a week. For example, if you only work on Mondays and Tuesdays, then a week of leave is 2 days. Your leave cannot start before the birth. It must end within 52 weeks of the birth (or due date, if the baby is early). The start and end dates rules are different if you adopt.

You must give your employer 28 days’ notice if you want to change your start date.

You do not have to give a precise date when you want to take leave. Instead you can give a general time, such as the day of the birth or one week after the birth.

Sick Leave

Statutory Sick Pay (SSP) is paid to employees who are unable to work because of illness. SSP is paid at the same time and in the same way as you would pay wages for the same period. Previously SSP was only payable from the 4th day of sickness, however from April 2026 the 3 waiting day period has been abolished. Employees are now entitled to receive SSP from the first full day of sickness absence.

The weekly rate of SSP from 6th April 2026 is £123.25 or 80% of the employee’s average weekly earnings, whichever is lower.

National Service

There is no compulsory national service in United Kingdom.

4. Taxation & Social Security

Tax & Social Security

The tax year runs from 6 April to 5 April the following year.

Income Tax

PAYE (Pay as You Earn) is the system that HM Revenue & Customs (HMRC) use to collect Income Tax and National Insurance contributions (NICs) from employees' pay as they earn it.

As an employer, you will have to deduct tax and NICs from your employees' pay each pay period and pay Employer's Class 1 NICs if they earn above a certain threshold. You pay these amounts to HMRC monthly or quarterly. If you do not send the correct amount, or if you send it in late, you may have to pay interest.

The amount you can earn before you start paying income tax (personal allowance) is £12,570 in tax year 2025/2026, and will remain the same for tax year 2026/2027. If you earn in excess of £100,000, then for every £2 you earn over £100,000, you lose £1 of personal allowance.

The income tax bands for the 2025/2026 and 2026/2027 tax years are different for the rest of the UK and for Scotland, and are as follows:

Rest of the UK Tax Rate:

| Tax Band | Tax Rate | Annual earnings |

|

Basic Rate |

20% |

£12,571 - £50,270 |

|

Higher Rate |

40% |

£50,271 - £125,140 |

|

Additional Rate |

45% |

Over £125,140 |

Scotland Tax Rates for 2026/2027:

| Tax Band | Tax Rate | Annual earnings |

|

Starter Rate |

19% |

£12,571 - £16,537 |

|

Basic Rate |

20% |

£16,538 - £29,526 |

|

Intermediate Rate |

21% |

£29,527 - £43,662 |

|

Higher Rate |

42% |

£43,663 - £75,000 |

|

Advanced Rate |

45% |

£75,001 - £125,140 |

|

Top Rate |

48% |

Over £125,140 |

This assumes individuals are in receipt of the standard Personal Allowance

Social Security

As an employer, you pay National Insurance contributions (NICs) on the earnings you provide to your employees. Earnings include not only cash amounts but also benefits, such as providing your employees with company cars.

Most workers (both employed and self-employed) also pay NICs on their earnings, in addition to Income Tax. Many of these contributions go towards building up workers’ entitlements to social security benefits such as Jobseeker’s Allowance and the State Pension.

The tax and NICs due on your employees’ earnings are calculated and deducted at the same time through the PAYE (Pay as You Earn) system when you operate your regular payroll. You then pay them to HM Revenue & Customs (HMRC). However, the NICs that apply to many employer-provided benefits are calculated separately after the end of the tax year. Please note, there is no separate NIC rate for Scottish or Welsh employees.

| Employee | 2026/27 |

| On earnings between £1,048.01 per month and £4,189 per month | 8% |

| On earnings above £4,189 per month | 2% |

The UK government introduced legislation, which requires all employers to enroll their workers into a qualifying workplace pension scheme if they are not already in one. All employers regardless of size have had to be involved in the scheme from October 2017 at the latest. The government has set a minimum percentage that has to be contributed with employer contributions being at least 3% and the total combined contribution being 8%.

Reporting

On a monthly basis, PAYE must be paid over to HMRC. This must reach HMRC by 22nd of the following month if paying electronically. If you operate PAYE (Pay as You Earn), there are a number of key tasks you must complete in the period around the end of the tax year on 5 April.

Under Real Time Information (RTI), reports are sent to HMRC in real time, so HMRC must be notified “on or before” each payment is made to employees or pensioners. Each employee still must be provided with a year-end P60 form summarizing their earnings and tax deducted in the previous tax year.

PAYE Settlement Agreement (PSA)

A PSA is an agreement with HMRC where a company agrees to meet some Income Tax and National Insurance liability on behalf of its employees. This is generally used where a company has paid for staff entertaining and doesn’t want their staff to have a tax liability on this benefit, although it can be used for relocation expenses (over the HMRC limit for allowable expenses) and other irregular items of expenditure to be agreed with HMRC.

5. Payroll Operations

Payroll

Reports

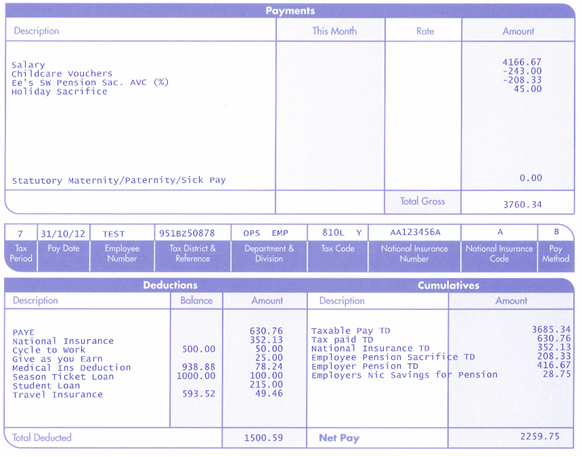

It is legally acceptable in the UK to provide employees with online payslips.

Payslip Example

Payroll reports must be kept for 3 years from the end of the tax year they relate to, however records relating to national minimum wage (NMW) compliance and redundancy payments must be kept for 6 years.

6. Hiring & Termination

New Employees

The employer will supply full details of the employee to HMRC via their payroll system when they submit their RTI file.

Leavers

When an employee leaves a company, the employer must complete a form P45 confirming:

- The leaving date

- Full name

- Home address

- National Insurance Number

- Date of birth

- Gender

- Works/payroll number

- The individual’s tax code

You also have to provide:

- Their overall pay and tax totals for the tax year so far, including from any previous employments during the year

- Their pay and tax figures relating only to their work for you during the tax year, if these differ from the employee's overall totals for the year

A copy of the P45 form is given to the employee. HMRC are notified that an employee has left a company by including a date of leaving in the next RTI submission.

7. Compensation & Benefits

Employee Benefits

(Embedded in social security: employer contributions to pensions, etc.)

Expenses

Expenses related to entertaining, relocation, and other irregular items can be handled via PSA agreements.

8. Visas & Work Permits

Visas & Work Permits

From 1 January 2020, ‘free movement’ in the EU ended and the UK’s new points-based immigration system began, which changed the way that employers hire most workers from outside the UK.

For recruitment purposes, EU and non-EU citizens are now treated equally. Employers are required to obtain a sponsor license to hire employees from outside the UK, with exceptions for Irish citizens and for some other immigration routes such as Global Talent.

FRONTIER WORKER PERMITS FOR EU CITIZENS

- Frontier Workers are individuals who work in one country while being primarily resident in another.

- Frontier Worker permits are mandatory from 1 July 2021 for all Frontier Workers except Irish citizens.

- UK Visas and Immigration will issue a Frontier Worker Permit to individuals who:

- Are a European Economic Area (EEA), European Union (EU) or Swiss citizen

- Are primarily resident outside the UK

- Have worked in the UK on or before 31 December 2020

- Have worked in the UK at least once in every 12-month period since beginning to work in the UK.

- Individuals who had not worked in the UK before 31 December 2020 and wish to work in the UK must apply for a visa (see 9.13.2 ‘Points-based immigration system’).

HIGH-VALUE MIGRANTS

- Investors, entrepreneurs and exceptionally talented people can apply to enter or stay in the UK without needing a job offer

- Individuals will need to pass a points-based assessment.

TEMPORARY WORKERS

- If an employer in the UK is willing to sponsor an individual, or if a citizen is from a country that participates in the youth mobility scheme, individuals may be eligible to come and work in the UK for a short period.

9. Location-Specific Considerations

- The UK has specific tax policies and reporting distinctions between Scotland and the rest of the UK, including different income tax bands.

- Post-Brexit, new visa systems such as Frontier Worker Permits are in place for EU workers.

- PAYE Settlement Agreements (PSAs) are specific tax arrangements used for staff benefits.

- Employers must comply with Real Time Information (RTI) submission rules on or before payroll date.

Further Information

For more information, or assistance with United Kingdom Tax inquiries please contact: gi@activpayroll.com

About This Payroll and Tax Overview

Please note that this document gives general guidance only and should not be regarded as an authoritative or complete statement of the law, regulations or tax position in any country. You should always seek specific advice for each specific situation. This document should not be relied upon as professional advice and activpayroll accepts no liability for reliance on its contents.